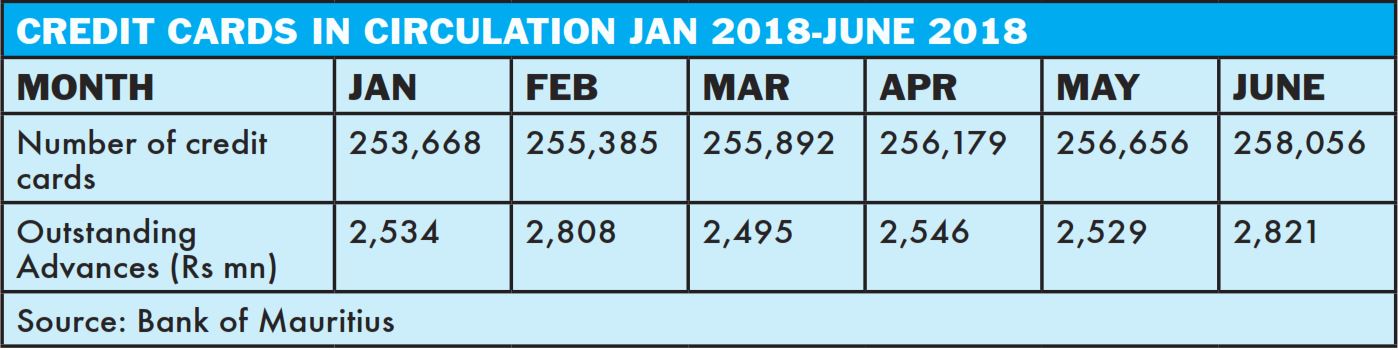

258,056 credit cards are in circulation as at June 2018. Going cashless surely helps us in our everyday life but at the same time, swiping the cards constantly and unconsciously can trap you into a vicious circle on financial instability. Are credit cards turning the new generation into money spending slaves, encouraging them to lead a lavish, deluxe lifestyle without any thought of saving for tomorrow?

Whether a common man or a professional, at some point in our life, we do overspend and find ourselves in a debt circle. But the new generation faces another type of temptation that the earlier generations were not exposed to, and therefore, they find it impossible to relate to: swiping of cards whenever they and wherever they want. There is no doubt that easy credit is omnipresent. Mauritius has witnessed major innovation in payment systems.

The number of credit cards has been witnessing an upward trend since 2000. As at June 2018, the number of credit cards amount to 258,056. According to statistical figures at the end of 2017, there were just above 255,000 credit cards in circulation within the Mauritian economy, roughly a ratio of 1 credit card for every 3 inhabitants (for an age range 15–60-years-old).

Similarly, while the number of credit cards are increasing, the outstanding advances on credits are also knowing an upward trend. Outstanding advances on credit cards were Rs 2,821 million at the end of June 2018 compared to Rs 2,420 million as at end-June 2017, representing an increase of 16.8% over the period. For the period end of June 2016, the outstanding advances were Rs 2,280 million. For the period June 2016 to June 2017, there was an increase of 6.1%. At the micro level, while the outstanding advances per credit card in circulation increased by 6.1 per cent from Rs 8,845 as at end-June 2016 to Rs 9,388 as at end-June 2017, the number of credit cards in circulation over the same period increased slightly by 0.03 per cent.

Daniel Essoo, Chief Executive Officer (CEO) of Mauritius Bankers Association (MBA), explains that Mauritius is a very small market with a high level of penetration/financial inclusion and credit cards segment is nearing maturity. “The growth in the credit cards volume is mainly due to the benefits and convenience of effecting payments with cards. More merchants are also accepting cards as a means to reduce the operational hassle involved with cash.”

He also reveals that banks are also enhancing the value propositions of their premium credit cards to include exclusive loyalty programme, offers and emergency assistance which includes comprehensive insurance covers, thus making credit cards very attractive. “Additional security features are being implemented to make internet purchases with credit cards more secure and to prevent any risk of fraudulent transactions. 24/7 online monitoring of transactions are being conducted by specialised teams to protect the cardholders.”

Vineet Jugessur, financial expert underlines that with changing lifestyles and growth in demand, credit cards have become inevitable today. “Apart from managing one’s financial needs, credit cards also prove to be one’s best friend in times of crisis. However, if used irresponsibly, one can easily be pushed into a debt trap.”

He avers that the demand for credit cards have been knowing a constant increase in recent years. The main drivers behind this increase, according to him, is mostly due to the following: shift in lifestyle, change in technology – trend is towards plastic money, increase in demand and consumption, improving job markets and increasing customer confidence, flexible access to short term credit.

According to a spokesperson from the Mauritius Commercial Bank (MCB), several factors contribute to this increasing need of credit cards. “First of all, all our MCB cards are safe and secured for usage. Security is a key aspect in all our cards, whether debit or credit or prepaid. It is noted that with the latest trend in Mauritian purchasing habits, our MCB credit cards are highly valued for online purchase. Upon transacting online, cardholders receive a ‘One Time Password,” known as OTP to validate their purchase.”

Change in doing shopping and business

The CEO of MBA confides that the usage of credit card is an easy, quick and secure way to pay your expenses without having to carry cash in hand. He lists the following changes occurred with the introduction of credit cards:

- Provides loyalty programmes such as discount offers, points or airmiles

- Enables safer and convenient Internet purchases

- Accepted worldwide and is very convenient during overseas travel

- Provides financial flexibility by offering interest free periods

- Offers flexible repayment options based on the customer’s repayment capacity

- Offers Insurance covers during travel and 24/7 Emergency assistance

- Reduced Administration Hassle especially during business travel

- Facilitates business and reduce the inconvenience of handling cash for merchants

Consequences on the economy

Vineet Jugessur underscores that used responsibly, a credit card can be a very helpful financial tool, granting people easy access to credit. “Making consistent and timely payments can lift credit ratings, whilst at the same time some cards also offer rewards on purchases. Moreover, credit card debt can also be a positive thing for the country’s economy. For instance, when people use credit cards to purchase goods and services, they may be using them as a means to finance purchases that they couldn’t otherwise afford. As a result, businesses boost up additional sales revenue they might not have otherwise received, hereby stimulating the economy.”

Unreasonable use on the other hand could lead to over dependency, resulting in negative consequences to both the users and the national economy, highlights the Financial Expert. “Certainly, consumers’ ability to finance new purchases can help the economy as a whole, but this effect has its restrictions. When credit cardholders over incur debt compared to their earnings, they end up having less spending ability, which can hurt the economy. Credit cardholders who carry outstanding balances must also bear high interest charges, which can ultimately reduce their purchasing capability.”

A debt trap

Sutyhudeo Tengur admits that credit card is a facility but not a real one as it is an enabler in putting people in more debts. “The credit card is not new. It has been in existence since several decades. It is a debt trap for those consumers who are not informed how to use this card responsibly. If you keep on using the credit card, you must know that the money that the bank is giving you through the credit card is a loan and the bank will deduct it with interests at the end of the month from your bank accounts. The interest rate is also very high – 2 per cent per month or 24% yearly. That makes a lot of money.”

He argues that from what we see around the super and hypermarkets, many consumers make use of this card to buy food items, or pay their restaurant bills. “As a responsible person, I say, if there is no money, don’t take your family out to the restaurant. Eat at home itself, meaning; “Cut your coat according to your cloth.” Don’t overdo. I know of people whose salary at the end of the month goes into paying back the bank the money they have used through their credit card. Such actions are making them poor.”

Sutyhudeo Tengur advises consumers to learn about the credit card from the internet, from an NGO, ask for detailed information from people who know, and why not from the bank itself about the interest rate, the card fee of Rs 250 charged every year from your bank account. “We do not encourage workers and middle-class people to get a credit card from the bank. Leave it for the rich Mauritians who can afford to throw money out of their window. I must also warn consumers about some banks that give away credit cards worth less than Rs 5000. This is a big debt trap which makes consumers who earn about Rs 10,000 a month, spend Rs 15,000 a month. Of course, there remains no money at all for savings for the future.”

Claude Canabady from the Consumers Eye Association, on his part, recalls that credit cards can get consumers into real financial difficulties especially if they do not pay off the money spent on the card in full every month. “They can encourage the consumer to buy things they cannot afford or items which are not essential at that moment in time and consequently, reduces future income which will be required to repay the credit card balance owed. The ability to delay paying off monthly balances can keep consumers in permanent debt. This is because consumers are encouraged by the credit card companies to pay off the outstanding minimum payment only. As long as the minimum amount is paid, the consumer can continue to spend up to their credit limit, therefore remaining in debt forever and paying high interest charges regularly.”

He puts forward that studies have highlighted that it is psychologically easier to spend more when paying with a credit card than when paying with cash. “It can also be tempting to spend more when some rewards are on offer.”

Vineet Jugessur also underlines that heavy burden of debts on people’s shoulders also affect the quality of their day to day life and this leads to further negative externalities to the society. “With their hidden charges and substantial interest rates, reckless cardholders can very quickly find themselves stuck in a debt trap and can take them a very long time, perhaps years, to detach themselves from this situation, provided that they are given the right guidance and advice.”

Michel Hardy, Vice-President of APEA (Association pour la Protection des Emprunteurs Abusés) contends we are unfortunately living in a society full of debts. “As time is passing by, the level of debts is increasing. Many households are submerged with debts. The banks easily convince people to get themselves a credit card. Promotions are fierce and people are easily influenced. However, consumers should know that banks will deduct their amount used automatically and the consumers will have to make adjustments for their living.”

Charges

There are various charges involved in the usage of credit cards and it is important for you to understand these charges. The following are the common charges that you may have to incur:

- The Annual Fee is a flat fee which is payable annually once you accept the credit card.

- The Finance charges (interest charges) are imposed by the credit card issuer on the outstanding balance which you have not settled on the due date.

- The cash advance fee is a fee charged for each cash advance transaction.

- You should be aware of the consequences of paying only the minimum repayment amount by the due date of each month. Not only will you incur more interest charges but also lengthen the time taken to repay your balance.

Shameema Gobindram-Namooya : “The big problem of credit cards is the interest rate”

Debt Recovery Specialist Shameema Gobindram-Namooya argues that the convenience of the credit card means the risk of getting into debt is too easy. “This is because mentally it’s harder to know how much you’re actually spending. It’s similar to your weight. A lot of time you may think you weigh more or less, but until you step on the scale, you really wouldn’t know. In the past, especially if I look at my elders, until they had enough money for something, they wouldn’t buy it. They were ‘cash buyers’.”

The psychology of taking physical money out of your wallet means mentally, you will be less inclined to spend frivolously, she says. “The big problem of credit cards is the interest rate. If you stick to paying back what you pay in one calendar month, the risk of adding the interest costs means paying off that debt takes longer and longer. I think the convenience of getting credit is the new way of getting in debt. Credit cards are just one of the many options out there.”

Common threats

Credit card surely facilitates your life but at the same time, it poses various threats. Daniel Essoo asserts that one of the main threat is card skimming. “There is a risk that the credit card could be skimmed. Card Skimming is the copying of encoded information stored on the magnetic stripe of a card by fraudsters, to create counterfeit cards to make illegal purchases and cash withdrawals. Besides, the credit card could be misused for online payment, whereby the card or the card data may be used to make unauthorized purchases and fraudulent transactions.”

As stated by the MCB, cardholders have the possibility to lose their card or have their card stolen. “If such a case arises, it is essential that the cardholder inform the Bank as soon as possible of the situation via our Contact Centre or visit one of our branches immediately. The card will have to be cancelled to prevent any further usage.”

Raj Appadu : “It is to the detriment of small businesses”

President of Common Front of Traders argues that credit card is beneficial for big shops and businesses rather than small shops or businesses. “We understand going cashless has its own safety but it is to the detriment of some our trades in Mauritius. If a person is spending more than Rs 1,000, he can swipe his card. But swiping a credit on a purchase of Rs 200 or Rs 500 is not beneficial for small businesses, as there is need to pay for a fee as well.”

Notre service WhatsApp. Vous êtes témoins d`un événement d`actualité ou d`une scène insolite? Envoyez-nous vos photos ou vidéos sur le 5 259 82 00 !

![[Document] Réforme électorale : découvrez les propositions du gouvernement](https://defimedia.info/sites/default/files/styles/medium/public/reform_electorale_document.jpg?itok=i-XvATtS)